- Summary:

- The Tesco share price could face additional downside pressure in may due to rising production costs for its suppliers.

The Tesco share price has lost its earlier gains on the day and now trades 0.18% to the downside. Tesco has struggled in recent trading sessions as declining consumer purchasing power starts to nibble at the sales volumes of the UK’s biggest supermarket chains. In addition, rising inflation has forced a 4th interest rate increase by the Bank of England, sending interest rates to the highest levels since 2009. But this may not impact the sales of Tesco and other supermarket brands immediately, given the recent industry numbers from NielsenQ.

Reuters is reporting that the trade body for the UK’s pig industry is asking Tesco to support its struggling members to prevent losing its UK supply base entirely. Rising feed prices to record highs are forcing pig producers to face unprecedented losses. A letter from the Chairman of the National Pig Association indicates that pig producers are selling at prices that are at least 15% below production costs. He called on Tesco to do more as the holder of a 27% market share of the UK’s grocery market.

The letter indicates the struggles being faced in the UK’s retail industry. Inflationary pressures are forcing consumers to substitute branded products for cheaper alternatives. The situation is dampening sentiment on UK supermarket stocks, leaving the Tesco share price stuck below the 275p mark.

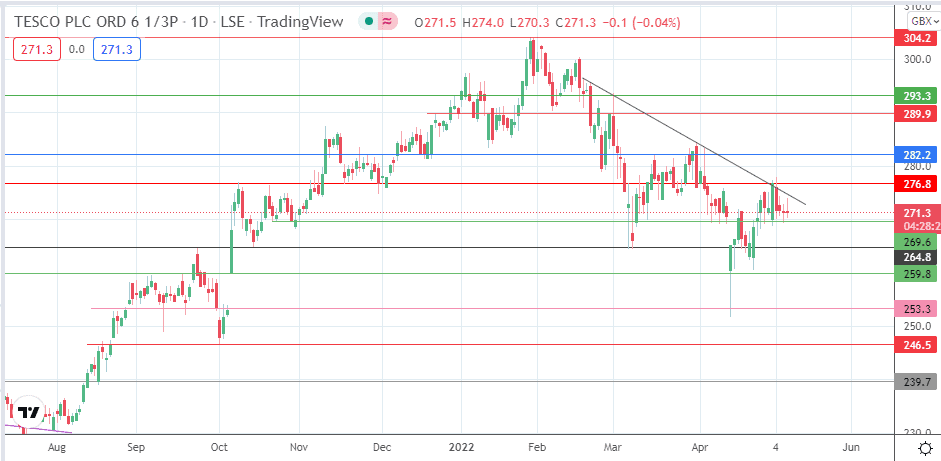

Tesco Share Price Outlook

The descending trendline that caps the recent tops from 15 February to date remains the barrier to break for the bulls. This trendline intersects the 276.8 resistance line, forming the major barrier that the bulls need to uncap to attain an advance towards 282.2 (1 December 2021 and 16 March 2022 highs). If the advance continues beyond this level, the 289.9 and 293.3 (1 March 2022) barriers are the next upside targets. 304.2 represents the 2022 high, and only when this resistance is broken will the uptrend resume, targeting 317.5 (27 October 2008 and 30 January 2012 lows in role reversal).

On the flip side, a further rejection at the trendline, followed by a degrading of the support at 269.6 (11 March, 12 April and 6 May lows), will open the door towards 264.8 initially (7 March low). This leaves the 259.8 support level (6 October 2021 and 25 April 2022 lows) as the next downside target. Further price deterioration allows 253.3 and 246.5 (1 October 2021 low) to enter the mix as potential pivots. 239.7 is another potential harvest point for aggressive bears pursuing a potential drop to this 17 August 2021 low.

Tesco: Daily Chart