- Tata Steel has been on an upside momentum for the most part since the year began, rising as the broader Indian equities market struggles

- The company recorded forecast-beating earnings with EBITDA rising 31% year-over-year

- Steel prices have been rising in India and China, with 12% government duty cushioning Tata from competition

It’s difficult to overlook Tata Steel’s spark if you’ve been following the Indian markets recently. The stock has recently brushed against its 52-week high of ₹211.39, after beginning the year with a strong 15% rally. We examine the factors driving this rally in an industry that has historically been thought of as cyclical and susceptible to changes in the price of commodities globally.

Why Tata Steel Is Rallying

There are two places where the heavy lifting is going on. Domestically, India’s steel market is a growth star. The World Steel Association projects that India’s steel consumption will increase by about 9% by 2026, despite the fact that the world’s steel demand is still slow. Due to record volumes in the automotive and retail segments, Tata Steel’s Q3 FY26 results showed a 31% year-over-year increase in consolidated EBITDA.

But Europe is the true surprise. The operations in the UK and the Netherlands were the portfolio’s top challenges for a long time. However, new data indicates that the Netherlands’ EBITDA has almost tripled and the UK’s losses have significantly decreased. The market is finally starting to factor in the protective moat that has been established by this operational shift and the Indian government’s 12% safeguard duty on steel imports.

According to a Zee Business article, hot-rolled coil (HRC) prices in India have gone up from about ₹47,500 per tonne in Q3 FY26 to about ₹53,500 per tonne in February 2026. This has had a big effect on realisations.

Safeguard duties on steel imports have helped protect domestic producers, while ongoing capacity expansions at Kalinganagar and other facilities are positioning Tata Steel to capture rising demand.

2026 Outlook and Key Risks

Tata Steel has a positive but challenging outlook for 2026. Earnings growth is anticipated to be driven by improved European profitability, capacity additions, and strong domestic demand. With the help of infrastructure and policy initiatives, analysts predict that India’s steel consumption will increase by 8–10% a year through FY30.

The ₹240 target set by Motilal Oswal suggests a 15% increase over the current price. But this momentum might be put to the test by threats of global overcapacity, especially from China, and possible fluctuations in the price of raw materials.

Tata Steel Stock Forecast

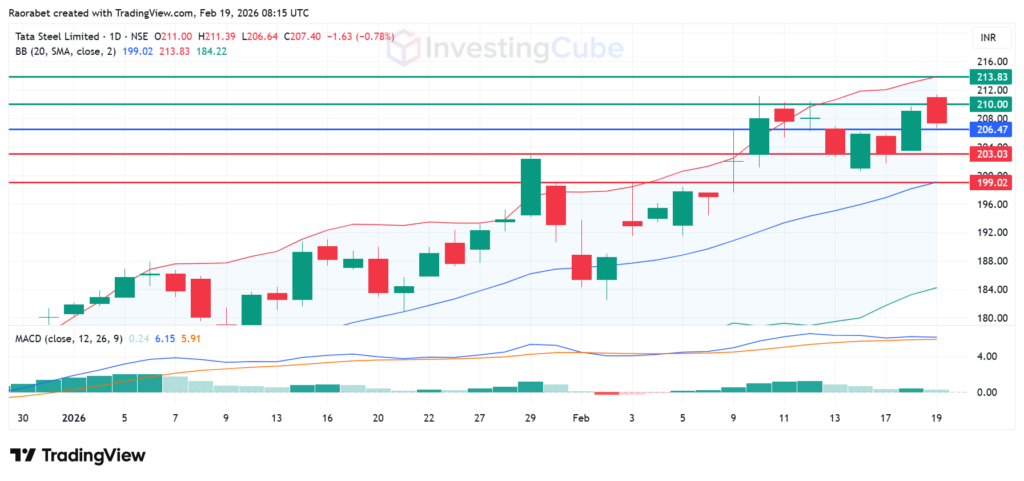

Tata Steel stock is currently trading at ₹207.40 and pivots at ₹206.47. The MACD is at 6.15, which is above the signal line and is a classic sign of a bullish trend. The stock is facing immediate resistance at ₹210. If it breaks above this level, it could start a run toward the upper Bollinger Band level at ₹213.83.

On the other hand, going below ₹206.47 will favour the sellers to take control. That will likely see the first support established at ₹203.03. Breaking below that level will signal a strong bearish momentum that could go on to test ₹199.01.

Tata Steel stock daily chart with key levels of support and resistance on February 19, 2026. Created on TradingView

The rally is due to a 31% rise in EBITDA for the third quarter of FY26, strong domestic demand in India’s automotive sector, and smaller losses in the UK as the company moves to more efficient ways of making things.

The Indian government’s 12% safeguard duty on steel imports acts as a catalyst. By making foreign steel more expensive, it protects Tata Steel’s domestic margins and allows for stable pricing despite global fluctuations.

The company will probably do well, with profits rising from new products and expansions, but the risks of exporting to China are still higher than many people think.