- Nvidia stock is down by more than 7%, a week after delivering another set of forecast-beating earnings

- The company also raised its guidance above market forecasts but the stock price signals concerns over valuation

- Delays in exporting chips to China has created a revenue bottleneck for Nvidia, but Vera Rubin platform could offer reprieve

It is a bit strange but it feels normal now, that Nvidia beats forecasts, lifts its outlook, yet still its shares slip. After reporting fourth-quarter numbers for fiscal 2026 in late February, with sales climbing to $68.1 billion, Nvidia stock has dropped about 7% across five sessions.

Is the Market Ignoring Nvidia’s Numbers?

Nvidia reported record Q4 revenue of $68.1 billion, a 73% jump from last year. Total yearly revenue hit $215.9 billion, up 65%. Data Center revenue set a record at $62.3 billion for the quarter, and Q1 FY2027 guidance is at $78 billion, above what analysts expected ($72.6 billion).

One might wonder why such strong numbers failed to propel the shares higher. While market consensus views this as a temporary pullback amid sustained AI demand, a unique perspective challenges this by noting early signs of customer concentration risks that could signal a plateau in growth sooner than anticipated.

Is Nvidia’s Medium-Term Outlook Under Threat?

That $78 billion forecast Nvidia gave for its first quarter, 77% higher than last year, quieted talk of a bubble, at least for now, according to Fortune. Still, how much customers are willing to spend may shift soon. J.P. Morgan analysts have pointed out uncertainty around data center growth in calendar year 2027. Some worry that hyperscalers’ cash flow issues could limit their spending.

AMD and Intel are providing more competition, with AMD’s MI300 series gaining ground. Geopolitical issues, such as export controls, also pose a threat to supply chains. Also, CEO Jensen Huang mentioned that Nvidia’s guidance assumes no revenue from China. The hidden downside is that Chinese companies like Huawei are stepping up.

By being locked out, Nvidia is effectively subsidizing the R&D of its future global rivals. Also, two customers accounted for 36% of Nvidia’s last quarterly sales, up from 34%, signaling concentration risks that could amplify if spending slows.

A rising concern often overlooked by equity analysts is the power grid. Estimates suggest nearly 25% of new data centers could sit idle due to electricity shortages. Nvidia can build the chips, but if the world can’t power them, the order book will eventually stall.

Meanwhile, the Vera Rubin platform ships in the second half of 2026 and it should cut inference token costs by up to 10x compared to Blackwell. That will extend the product cycle and give hyperscalers a reason to keep spending. The GTC conference in March should have major product releases, which could reset the stock’s sentiment soon.

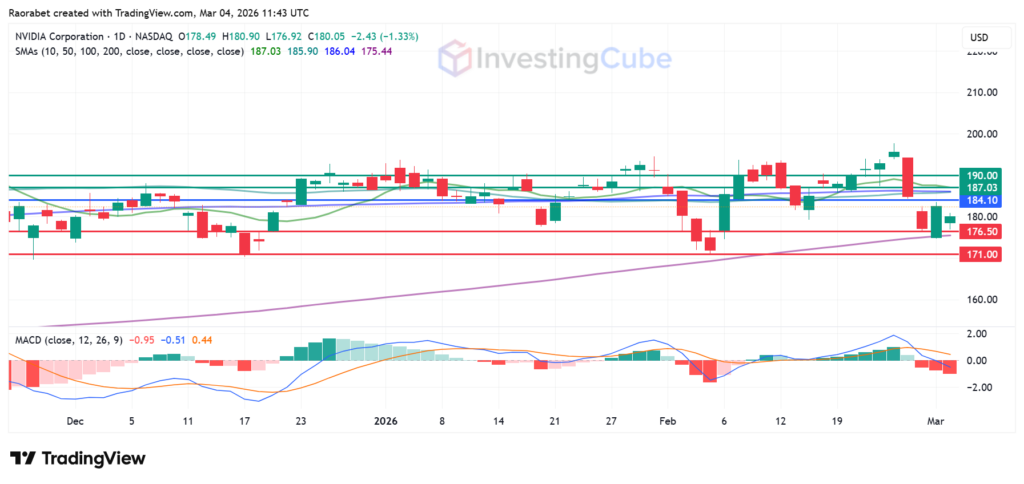

Nvidia Stock Price Forecast

After the post-earnings slide, the stock pivots at $184.10 and its immediate resistance is at the 10-day Simple Moving Average (SMA), situated around $187.03. A break above that will target $190. Immediate support lies at $176.50. A sustained close below this could open the trapdoor toward $171, near YTD lows.

Nvidia stock daily chart on March 4, 2026 with levels of key support and resistance. Created on TradingView

Investors had already priced in a massive beat. When the results were merely excellent rather than miraculous, traders took profits.

Yes, but not because of low demand. The issues are execution and infrastructure. The main risks are power grid issues that stop new data centers from opening and revenue being heavily dependent on five cloud customers.

Nvidia’s market share in China has basically dropped to 0% because of U.S. export restrictions. Even though this is priced in, the long-term risk is that Chinese companies now have to build their own AI ecosystem.