GBPUSD

The Pound has pared some of yesterday’s losses this Tuesday, as the cable tries to make sense of the new national lockdown announced yesterday by the UK government. The new nationwide lockdown in response to the rapid spread of the new coronavirus variant prompted a selloff on the GBPUSD yesterday. However, this downside move is being rejected by bulls on the pair.

Today’s announcement by Chancellor of the Exchequer Rish Sunak on the inclusion of the next round of coronavirus economic support in the March budget (as per Reuters) is what has driven bullish action on the pair this Tuesday. However, bulls continue to struggle to return the cable to the year’s starting highs.

With the country now in the post-Brexit phase, the fundamentals for the cable have tilted towards the economic impact of the coronavirus epidemic.

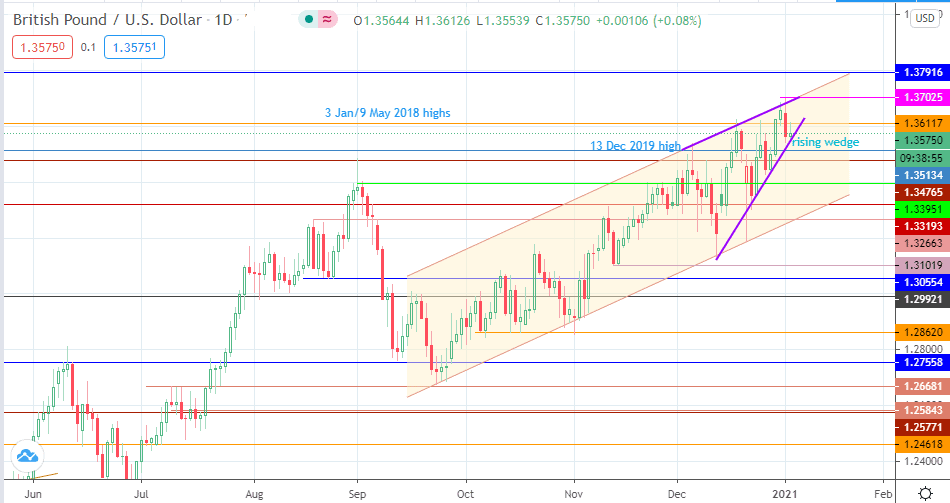

The pair has formed a rising wedge on the daily chart. The lower edge of the wedge provided support to bullish action on the day, but this has met resistance at the 1.36117 price level. This resistance must be overcome for bulls to attain the wedge’s upper boundary at 1.37025 (4 Jan high), with 1.37916 also forming a target to the north.

On the flip side, a pullback from the current resistance puts the wedge’s lower boundary at risk, with 1.35134 and 1.34765 serving as the immediate downside targets. If the downside move is a breakdown of the wedge pattern, then the measured move could target 1.33951 as well.

{kind=link}